Greece is about to receive its third multibillion euro bailout in just 5 years. With this lifeline, the Greek people faces a fresh wave of austerity policies – increase in taxes, public sector wage cuts, more cuts in pension benefits – basically the same approach has been tried repeatedly with no results to show for.

The fairy tale (tragedy) started when Greece joined the Eurozone in 2001. Becoming part of a developed region, the Greek economy boomed with confidence and prosperity. Everything went to shits in 2008 during the global financial crisis. The entire Europe entered a recession, but Greece was hit particularly hard as it is one of the poorest, least industrialized, and most heavily-indebted countries. Unemployment rate reached 28% in 2013, worse than the US during the Great Depression.

I. How much do the Greeks owe?

Technically debt is 177% of GDP -- twice the level of the US. However, deep depression – real GDP contraction of 26% over the past 6 years – means it has no way of raising capital, so the debt situation will only get worse and worse. Any tax hikes or budget cuts to help pay debt would just worsen the depression.

Looking at it this way, the debt level is just an academic exercise: it's sort of like saying "I'm super broke" instead of "I'm deadbeat broke".

But it was in no way sustainable. A sharp reversal followed.

1) It's the Greeks' own fault

Since Greece reinstated democracy in 1974, the country's bureaucracy has been grown fatter and fatter, with each new administration adding its supporters to the public sector payroll — and wages rising steeply in the past decade. Economist Yannis Stournaras: “The government kept adding bonuses and benefits and pensions. At election time there was a boom cycle as they handed out jobs.”

There were rampant cases of waste and abuse of power among bureaucrats, including officials who hire their wives, or $750k/year office space just for 11 people. It was a bureaucracy which employs one out of five workers in the country, with nearly 800,000 public sector employees. The government is basically an army of patronage appointments, campaign workers, built up over decades; they also have lifetime tenure and indifferent to productivity.

The national budget has more holes than Swiss cheese. Shipping, which contributes 7% to the country’s GDP, is nearly exempt from taxes or duties, and income from international business aren't taxed at all. At the same time, tax evasion by Greek citizens and businesses remains a huge problem. The average taxpayer only report half of their real income. Tax evasion accounted for half of the country’s 2008 deficit and a third of its 2009 deficit. And there has been no signs of reforms on this front, despite the obvious need.

2) European leaders completely mishandled the situation

Some critics blame Europe for providing the first two bailouts. Europe, they argue, has been unwilling to accept fault for lending so much bad loans to the poor nation.

This is akin to blaming thieves after you left your front door wide open.

The argument for the first and second bailout was clear: the world is in the midst of a debt-fueled financial crisis, and any sovereign failure can be systemic – just like Lehman was. The Greek rescue package was necessary to keep the financial system running, while proper monitoring and safeguards are installed into place. Since 2010, the EU has set up a permanent bailout fund, stiffened deficit- and debt-limitation rules, tightened surveillance of national economies to prevent asset bubbles, centralized bank regulation and — perhaps most important — allowed the ECB to act as a safety net for unhinged economies.

However, the creditor group’s mismanagement of the Greek problem meant that the second, third, and likely more bailout rounds would be needed. The “Troika” of creditors – the ECB, the EU commission and the IMF – told Greece to adopt severe austerity, which felt to Greeks like the shredding of labor rights and benefits. This program not only failed to make the debt sustainable; it has carried the country backwards to the pits of poverty.

Meanwhile, the bulk of the €240bn rescue funds Greece received in 2010-2012 went straight back to the banks that lent it money before the crash.

3) The bankers are the devil

For years, Goldman Sachs and JPMorgan helped Greece, Italy and other sovereign governments, to hide mountains of bad loans within structured products -- similar to what eventually triggered the subprime mortgage crisis. The schemes are not illegal, but they completely distort the government balance sheet and hide the real picture from Eurozone statisticians and policy makers.

The discrepancy turned out to be massive. In November 2009, newly-elected PM George Papandreou admitted that the year's budget deficit would be 12.7% of GDP, almost quadruple the 3.7% the previous government projected. The country's finances were in much rougher shape than anyone — especially anyone buying Greek bonds — had realized.

4) The Syriza government is at fault

The Greek political landscape has traditionally been dominated by two parties, PASOK and New Democracy; the duopoly – and the race to buy votes in every election – was partly the cause of the problem as previously mentioned. Desperate for a change, in January 2015 the citizens elected the far-left party Syriza led by PM Alexis Tsipas on a platform of ending austerity.

So it wasn’t the party’s fault that the economy is in shambles; it simply inherited a mess already brewing for decades (by making promises it probably can't keep).

However, Tsipras’ behavior during the bailout negotiations ticked off many. The rhetoric coming from Athens is as heated; there is even talk of European “blackmail” against the free will of Greek voters, as if Germany and France don’t have voters of their own.

Tsipras was unable to come up with proposals that secure support from any substantial number of other European governments, leading to a deadlock. Then on June 30, he stopped talks to hold a referendum, asking the population to reject the creditors’ terms, just to later accept an even tougher terms of austerity. He framed the referendum question as: “do you want to keep using the euro?”, which is like asking, “do you want to lose your life savings now for the sake of uncertain (maybe better but still uncertain) future, or don’t lose your savings now but with an uncertain future as well?” And the people have decided: they don’t want to lose their savings. Can you blame them?

In essence, months of brinkmanship has caused untold damage to the Greek economy for no purpose whatsoever.

Italy also took the pill and probably needs 20 years to rebuild and regain its job market. Even Bulgaria, which only joined the EU in 2007 and is still trying to get into shape to adopt the common currency, is fed up. “We are much poorer than the Greeks, but we have performed reforms,” President Rosen Plevneliev pleas. The Ukrainian people, ailing from an armed conflict with neighboring Russia, sees Greek pensioners’ high living standards with disdain.

Even the reviled IMF can explain its hard line: given the bitter programs it has imposed on other countries (Indonesia, South Korea, and Thailand in 1997-98, just to name a few), it can hardly now be lenient towards a more developed and relatively better off European country. Actually the Asian Financial Crisis sets a pretty good precedent as there are many similarities to the Greek situation, as well as lessons to be learned.

If Greece were allowed to run a budget deficit and create fiscal stimulus to offer jobs and relief to the most desperate citizens, then its social crisis would lift. But the terms of the bailout package won't allow any of this – Tsipras already agreed to target an aggressive 3.5% budget surplus (excluding debt service) in pre-bailout talks, meaning more belt-tightening as if there are any notches left.

In fact, this bailout, just like previous ones, only buys time for Greek people and other lenders to exit before things get worse. Much of the previous rescue funds have gone to pay off Greek bonds held by private investors and other eurozone governments, rather than on programs to stoke growth. The money was supposed to help replenish banks’ capital, to get them lending to revive the moribund economy. Instead, it sat in banks’ coffers as bad debts piled up, and it bought time for Greeks and foreign investors to get their money out. Only $27b out of the $230b of bailouts have gone to government spending, the rest mostly went to debt repayments and interest payments and commercial banks.

Furthermore, one of the bailout provisions prescribes selling off Greek state assets (companies, utilities, airports and whole islands) and generating about $55 billion in revenue, half of which would go toward debt service. The idea of a public garage sale was part of the previous rescue programs — and failed miserably. Only a fraction of the projected amount was raised, and hardly anyone expects much more this time around. Furthermore, years of economic hardship has damaged the value of domestic assets, that's assuming there are still buyers left.

Even Wolfgang Schaeuble, the German finance minister, is on record saying that a temporary "timeout" for Greece from the euro would in many ways be preferable to a new rescue package.

II. How badly has it affected the Greek people ?

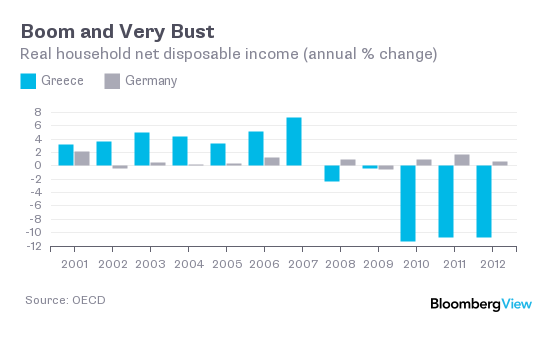

The economic contraction continues thru this year, with GDP growth estimated to be -4%. The Greeks have surely suffered, but to many outsiders (i.e. northern Europeans), the country is where it should have been without the confidence boost when they entered the Eurozone. Adopting the Euro, and being able to borrow massive amounts on the cheap, created a boom for Greek personal wealth. A lot of it was surely misdirected through reckless spending and corruption, but a boom nonetheless.

But it was in no way sustainable. A sharp reversal followed.

III. Whose fault is it really?

There’s plenty of blame going around. If you give me more fingers and I’ll point them at more culprits.1) It's the Greeks' own fault

Since Greece reinstated democracy in 1974, the country's bureaucracy has been grown fatter and fatter, with each new administration adding its supporters to the public sector payroll — and wages rising steeply in the past decade. Economist Yannis Stournaras: “The government kept adding bonuses and benefits and pensions. At election time there was a boom cycle as they handed out jobs.”

There were rampant cases of waste and abuse of power among bureaucrats, including officials who hire their wives, or $750k/year office space just for 11 people. It was a bureaucracy which employs one out of five workers in the country, with nearly 800,000 public sector employees. The government is basically an army of patronage appointments, campaign workers, built up over decades; they also have lifetime tenure and indifferent to productivity.

The national budget has more holes than Swiss cheese. Shipping, which contributes 7% to the country’s GDP, is nearly exempt from taxes or duties, and income from international business aren't taxed at all. At the same time, tax evasion by Greek citizens and businesses remains a huge problem. The average taxpayer only report half of their real income. Tax evasion accounted for half of the country’s 2008 deficit and a third of its 2009 deficit. And there has been no signs of reforms on this front, despite the obvious need.

2) European leaders completely mishandled the situation

Some critics blame Europe for providing the first two bailouts. Europe, they argue, has been unwilling to accept fault for lending so much bad loans to the poor nation.

This is akin to blaming thieves after you left your front door wide open.

The argument for the first and second bailout was clear: the world is in the midst of a debt-fueled financial crisis, and any sovereign failure can be systemic – just like Lehman was. The Greek rescue package was necessary to keep the financial system running, while proper monitoring and safeguards are installed into place. Since 2010, the EU has set up a permanent bailout fund, stiffened deficit- and debt-limitation rules, tightened surveillance of national economies to prevent asset bubbles, centralized bank regulation and — perhaps most important — allowed the ECB to act as a safety net for unhinged economies.

However, the creditor group’s mismanagement of the Greek problem meant that the second, third, and likely more bailout rounds would be needed. The “Troika” of creditors – the ECB, the EU commission and the IMF – told Greece to adopt severe austerity, which felt to Greeks like the shredding of labor rights and benefits. This program not only failed to make the debt sustainable; it has carried the country backwards to the pits of poverty.

Meanwhile, the bulk of the €240bn rescue funds Greece received in 2010-2012 went straight back to the banks that lent it money before the crash.

3) The bankers are the devil

For years, Goldman Sachs and JPMorgan helped Greece, Italy and other sovereign governments, to hide mountains of bad loans within structured products -- similar to what eventually triggered the subprime mortgage crisis. The schemes are not illegal, but they completely distort the government balance sheet and hide the real picture from Eurozone statisticians and policy makers.

The discrepancy turned out to be massive. In November 2009, newly-elected PM George Papandreou admitted that the year's budget deficit would be 12.7% of GDP, almost quadruple the 3.7% the previous government projected. The country's finances were in much rougher shape than anyone — especially anyone buying Greek bonds — had realized.

4) The Syriza government is at fault

The Greek political landscape has traditionally been dominated by two parties, PASOK and New Democracy; the duopoly – and the race to buy votes in every election – was partly the cause of the problem as previously mentioned. Desperate for a change, in January 2015 the citizens elected the far-left party Syriza led by PM Alexis Tsipas on a platform of ending austerity.

So it wasn’t the party’s fault that the economy is in shambles; it simply inherited a mess already brewing for decades (by making promises it probably can't keep).

However, Tsipras’ behavior during the bailout negotiations ticked off many. The rhetoric coming from Athens is as heated; there is even talk of European “blackmail” against the free will of Greek voters, as if Germany and France don’t have voters of their own.

Tsipras was unable to come up with proposals that secure support from any substantial number of other European governments, leading to a deadlock. Then on June 30, he stopped talks to hold a referendum, asking the population to reject the creditors’ terms, just to later accept an even tougher terms of austerity. He framed the referendum question as: “do you want to keep using the euro?”, which is like asking, “do you want to lose your life savings now for the sake of uncertain (maybe better but still uncertain) future, or don’t lose your savings now but with an uncertain future as well?” And the people have decided: they don’t want to lose their savings. Can you blame them?

In essence, months of brinkmanship has caused untold damage to the Greek economy for no purpose whatsoever.

IV. The rest of the world really hates Greece

It’s not just Germans who are tired of Greece. Leaders in Spain, Ireland, and Portugal – Eurozone’s poorest countries– have been Greeks’ toughest critics; they argue that their countries swallowed the harsh austerity medicine after the debt fallout and that Greece must, too.Italy also took the pill and probably needs 20 years to rebuild and regain its job market. Even Bulgaria, which only joined the EU in 2007 and is still trying to get into shape to adopt the common currency, is fed up. “We are much poorer than the Greeks, but we have performed reforms,” President Rosen Plevneliev pleas. The Ukrainian people, ailing from an armed conflict with neighboring Russia, sees Greek pensioners’ high living standards with disdain.

Even the reviled IMF can explain its hard line: given the bitter programs it has imposed on other countries (Indonesia, South Korea, and Thailand in 1997-98, just to name a few), it can hardly now be lenient towards a more developed and relatively better off European country. Actually the Asian Financial Crisis sets a pretty good precedent as there are many similarities to the Greek situation, as well as lessons to be learned.

V. There are many advocates of Grexit

Economically speaking, there is a wealth of arguments for Grexit. For one, reviving growth was never the primary sticking point during the powwow with the Troika – it always revolved around austerity measures and debt repayment.If Greece were allowed to run a budget deficit and create fiscal stimulus to offer jobs and relief to the most desperate citizens, then its social crisis would lift. But the terms of the bailout package won't allow any of this – Tsipras already agreed to target an aggressive 3.5% budget surplus (excluding debt service) in pre-bailout talks, meaning more belt-tightening as if there are any notches left.

In that sense, many argue that leaving the euro may just be the best option left. In the short term, this would be a rough path. Greece would suddenly become a poor, isolated failed state stuck between richer northern Europe and conflict-stricken Africa and Middle East. Access to external funding sources would disappear overnight. Very stringent capital controls would be needed to keep banks solvent. A lot of personal wealth would be wiped out as the value of drachma-denominated assets plummet. Dangerous inflation may arise. It would probably look a lot like the Soviet Union circa 1991.

But Grexit at least provides the country with a path back toward growth sometime in the next decade. The Greek people would finally have control over their monetary policy, letting them devalue their currency, boost exports and tourism, and get back on track.

Politically, it’s a totally different ball game. Nobody really knows what the political cost of Grexit will be. Angela Merkel subscribes to Helmut Kohl’s ideology, that the EU needs to show the world that it can remain united in the face of difficult internal issues – especially with looming threats from Putin's militaristic ambitions and sectarian violence in the Middle East and Africa along with the migrant influx and humanitarian situations. Merkel, Hollande and others, they are children and grandchildren of the WWII, and nobody wants to relive those painful childhood memories.

But Grexit at least provides the country with a path back toward growth sometime in the next decade. The Greek people would finally have control over their monetary policy, letting them devalue their currency, boost exports and tourism, and get back on track.

Politically, it’s a totally different ball game. Nobody really knows what the political cost of Grexit will be. Angela Merkel subscribes to Helmut Kohl’s ideology, that the EU needs to show the world that it can remain united in the face of difficult internal issues – especially with looming threats from Putin's militaristic ambitions and sectarian violence in the Middle East and Africa along with the migrant influx and humanitarian situations. Merkel, Hollande and others, they are children and grandchildren of the WWII, and nobody wants to relive those painful childhood memories.

VI. This round of bailout and any future rounds –and there will be– will not be sufficient

The Greek economy is too damaged, and the debt burden is too heavy. Debt forgiveness, not just rollovers, will be needed. In essence, Europe needs to admit that they had royally fucked up in the way they handled the issue.In fact, this bailout, just like previous ones, only buys time for Greek people and other lenders to exit before things get worse. Much of the previous rescue funds have gone to pay off Greek bonds held by private investors and other eurozone governments, rather than on programs to stoke growth. The money was supposed to help replenish banks’ capital, to get them lending to revive the moribund economy. Instead, it sat in banks’ coffers as bad debts piled up, and it bought time for Greeks and foreign investors to get their money out. Only $27b out of the $230b of bailouts have gone to government spending, the rest mostly went to debt repayments and interest payments and commercial banks.

|

| Wanna buy a Greek island? |

Furthermore, one of the bailout provisions prescribes selling off Greek state assets (companies, utilities, airports and whole islands) and generating about $55 billion in revenue, half of which would go toward debt service. The idea of a public garage sale was part of the previous rescue programs — and failed miserably. Only a fraction of the projected amount was raised, and hardly anyone expects much more this time around. Furthermore, years of economic hardship has damaged the value of domestic assets, that's assuming there are still buyers left.

VII. Many stakeholders –even the creditors– don't believe Greece can get back on its feet

The IMF estimates that even if Greece achieves all the reforms (note: that’s a huge if), debt-to-GDP will only come down to a still-unsustainable 118% by 2030.Even Wolfgang Schaeuble, the German finance minister, is on record saying that a temporary "timeout" for Greece from the euro would in many ways be preferable to a new rescue package.

VIII. The real homework for Greece is to fix its fundamentals and business environment

Greece has an entrenched system and regulations molded over decades to protect incumbents and stifle innovation, entrepreneurship and new business models. As a result, inefficiencies abound and the country suffers from poor productivity and a dearth of talent. To restore the economy, the country must focus on the basics: stability, investment and simpler laws. This is Econ 101 stuff. There are still prospective sectors that may lead future growth for the nation: tourism, shipping, agriculture, and pharmaceutical industries just to name a few.

Professor Michael G. Jacobides of the London Business School: "...on balance the structural changes that the deal calls for represent a once-in-a-lifetime opportunity. They are reforms that no government in Greece, including Syriza, has attempted, for fear of upsetting powerful vested interests. By forcing the government to remove institutional barriers to competition and innovation the deal will create a sound basis for economic growth and development. If (and that’s a huge if) the politics work out, confidence returns, and people invest again, things could get back on track; the alternative may be a failed state. So, let’s keep a cool head, and not throw the baby out with the bathwater. There’s just too much at stake—for Greece, for the Eurozone, and for the European project more broadly."

Professor Michael G. Jacobides of the London Business School: "...on balance the structural changes that the deal calls for represent a once-in-a-lifetime opportunity. They are reforms that no government in Greece, including Syriza, has attempted, for fear of upsetting powerful vested interests. By forcing the government to remove institutional barriers to competition and innovation the deal will create a sound basis for economic growth and development. If (and that’s a huge if) the politics work out, confidence returns, and people invest again, things could get back on track; the alternative may be a failed state. So, let’s keep a cool head, and not throw the baby out with the bathwater. There’s just too much at stake—for Greece, for the Eurozone, and for the European project more broadly."